|

|

The Lone Star Letter

February 2021

|

|

|

|

|

|

|

New Investment Opportunity

We launched our latest investment opportunity last week. Click below to access our investment portal to learn more:

|

|

|

|

|

|

|

New Webinar Series

I'm excited to start doing live webinars and share screen to dive deeper into specific topics each week/month (frequency TBD). Click the link below to register for the upcoming webinar:

|

|

|

|

|

|

|

|

|

|

What it Takes to Cash-Out Refi

Many investors, beginner and experienced, are enamored with the strategy of buying a value-add deal, raising the value of the property, then doing a cash-out refinance to return 100% of the originally invested equity. While this is a tremendous strategy as it is not only a great way to generate outsized returns and build a growing portfolio, but also extremely tax-efficient, since a refinance is not a taxable event.

However, 100% cash-out refinances are not a common occurrence today even on a heavy value-add deal, since prices are high and takeout leverage is constrained to around 75% (except HUD 223(f) loans which can be levered up to 83%). Stabilized core-plus or value-add deals are nearly impossible to pull off a 100% cash-out refi, not only because prices are high, but also because this deal strategy and financing strategy are a mismatch.

The reality is value must be increased so substantially through the business plan and potentially through appreciation (which can come in the form of rent increases or cap rate compression) that the total capitalization of the deal must be 75% or less of the new appraised value on a refinance. This math makes logical sense since you would have to get a 75% LTV loan based on the new value of the property and use those new loan proceeds to pay off the old debt as well as return all of the original equity (making up the deals acquisition total capitalization).

Let’s take a deeper dive into these numbers and really look at the metrics of a deal that would produce this level of value increase, such that a 100% cash-out refinance is a potential reality.

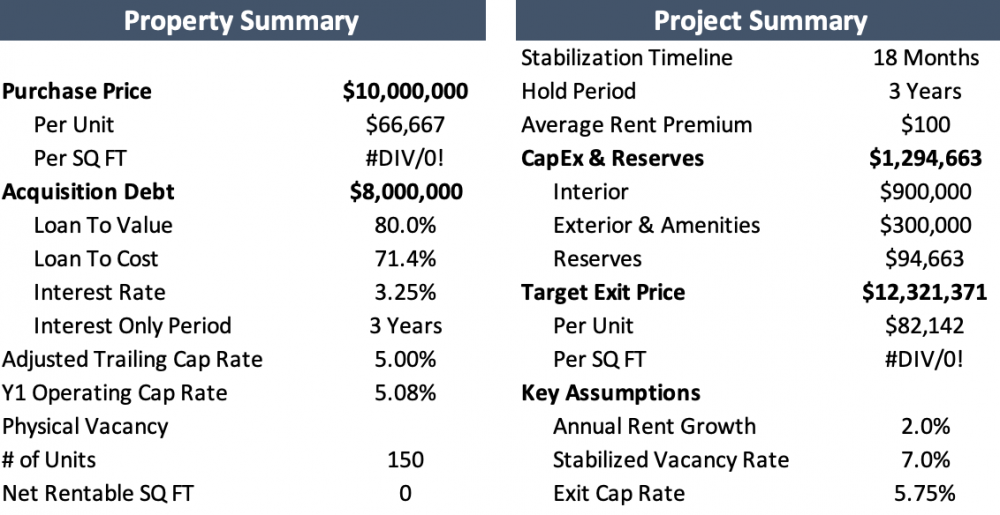

Here we have an example 150-unit multifamily deal we will use to draw conclusions about the qualities of a deal which make it more likely to achieve a full cash-out refi:

|

|

|

|

|

|

|

|

|

As you can see, this is a very prototypical value-add deal. The property is being purchased at a 5% cap rate and the capex budget is $8k/u for both interior and exterior upgrades in order to achieve a $100 rent premium, resulting in a 12.5% revenue increase. For this hypothetical deal, we are keeping expenses the same from in-place to pro forma.

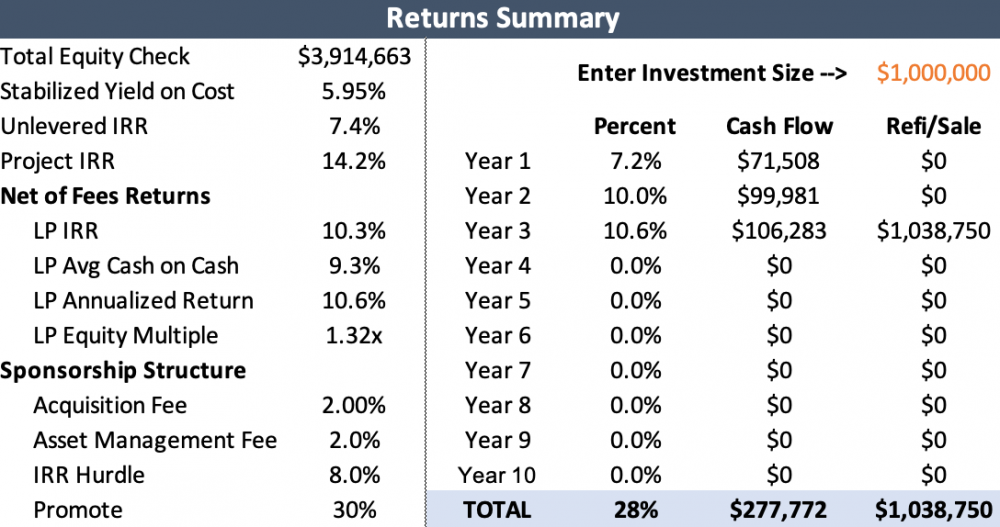

We are assuming 80% going-in leverage on a Freddie Mac floating rate loan which only has a 1% prepayment penalty, allowing for an economical refinance. The projected returns are 14.2% gross IRR over a 3-year hold which is in-line with market averages for a value-add deal of this profile today. The stabilized yield on cost is 5.95%.

Now if we project a refinance after 24 months of ownership after the value-add business plan is complete (assuming an 18-month stabilization period to raise rents on all 150 units), the cash-out would be about 35%. This is assuming 75% LTV on the new loan and a refi cap rate of 5.5%.

|

|

|

|

|

|

|

A 35% cash-out is certainly a major success, but still nowhere near the 100% target. Furthermore, this is assuming there is no cap rate expansion in the refinance valuation and no interest rate increases which may hurt leverage through debt service coverage ratio constraints.

So, how much more value would need to be created from a revenue growth and return on cost perspective to pull off a 100% cash-out? If we increase the rent increase from $100 to $150, that raises the total revenue increase to 18.3% which results in an impressive return on cost of 6.64%. if you’re not familiar with the return on cost metric or its significance, check out this article here.

Now this hypothetical deal is achieving a terrific 24.4% project IRR over a 3-year hold, assuming a 5.75% exit cap rate. However, a 24-month refi at a 5.5% cap rate valuation still only gets us to 62% cash-out. Still a long way to go to 100%! The metrics on the deal look great now but still not good enough for every investor’s favorite: a 100% cash-out refinance.

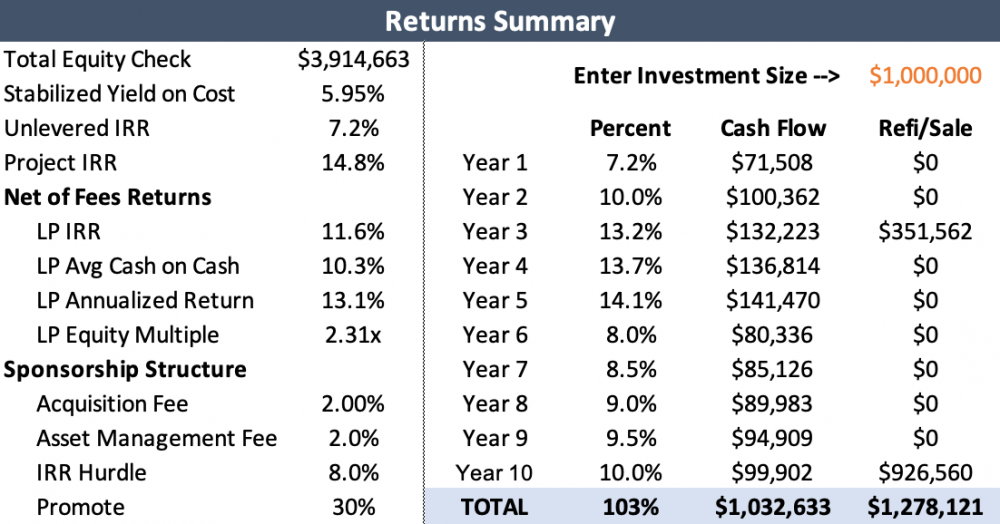

Lastly, let’s try raising rents by $225 through our $8k/unit capital expenditures program. This is a far cry from our original $100 increase scenario and experienced investors know that finding any deal where you can raise rents $225 is very difficult. Furthermore, it is not just about how much you raise rents since you’re going in valuation matters and, even more important, is your return on cost. For example, you could find a deal where you can raise the rents by $225 but you may have to pay a 3% going-in cap rate for the deal, since the market is pricing in the upside, limiting the upside.

With $225 rent increases, the resulting revenue increase is a whopping 27.1% and a stabilized return on cost of 7.68%. These deal metrics result in an unbelievable 37.3% gross IRR over a 3-year hold. Finally, we are also able to achieve a 103% cash-out refi. This goes to show you just how difficult it is to achieve a 100% cash-out refi and therefore should not be relied upon as a viable strategy in most circumstances. Nevertheless, supplemental loans and refinancing are powerful tools even if they only result in a small cash-out.

In conclusion, investors should generally have more realistic expectations in regard to cash-out refinances in today’s market. Furthermore, investors should not expect that a cash-out refi is a good short-term strategy for cash flow deals which are better suited for long-term holds. We continue to seek deals at both ends of the spectrum; deep value-add opportunities which may deliver high-teens returns and approach the 100% cash-out refi threshold (but we won’t base our assumptions on that), and core-plus deals characterized by quality assets in quality locations, which exhibit a strong and growing cash flow opportunity.

|

|

|

|

|

|

|

Capital Spotlight Podcast

The Capital Spotlight podcast interviews capital allocators and intermediaries to learn more about their strategies, sponsor and investment criteria, due diligence process, and asset management practices. You can check out the podcast here.

|

|

|

|

|

|

|

We Seek Opportunity

Lone Star Capital acquires B/C multifamily properties in Texas and throughout the Southeast. We seek true value-add opportunities that are under-managed, have high vacancy, below market rents, and deferred maintenance. We underwrite quickly and make prompt, confident offers. Please reach out if you have an opportunity you believe would be a good fit for us. Click here to view Lone Star's Acquisition Criteria.

Work With Us

We are always looking to build new relationships with co-GPs and equity partners. Reply to this email if you would like to discuss our current pipeline of deals and how we may best work together.

Lone Star Capital provides preferred equity for sponsors seeking to grow their business. Lone Star’s preferred equity product allows a multifamily sponsor to retain maximum profits with a cost-effective alternative or supplement to equity capital for acquisition and recapitalization. As an owner-operator, Lone Star understands the needs of sponsors and can better tailor terms based on the deal profile and goals of the sponsor. Click here to view Lone Star’s Preferred Equity Tear Sheet. Please reply to this email if you have a deal seeking preferred equity or would like to learn more.

Lone Star Capital can help you get your deal done. Lone Star acts as a co-GP for emerging sponsors seeking a loan guarantor to satisfy lender net worth, liquidity, and experience requirements.

Click here to download Lone Star's Underwriting Model.

About Lone Star Capital

Lone Star Capital is a real estate investment firm focused on acquiring underperforming multifamily properties in Texas. Lone Star delivers superior risk-adjusted returns by implementing moderate to extensive renovations, improving management, and designing creative capital solutions. In addition, Lone Star provides preferred equity and capital markets advisory to multifamily sponsors nationwide. Lone Star owns over $100MM of multifamily properties throughout Texas and the Southeast. Click here to view Lone Star's Company Presentation.

|

|

|

Robert Beardsley, Principal

(650) 380-2609

Rob@lonestarcapgroup.com

|

|

|

Kent Piotrkowski, Principal

(917) 744-9482

Kent@lonestarcapgroup.com

|

|

|

|

|

|

|